Capitalizing on Global Listed Infrastructure Investments

The Global Listed Infrastructure (GLI) universe continues to emerge as an investment strategy for investors seeking inflation-sensitive assets with the potential to deliver equity-like returns. Alongside other real assets such as midstream MLPs, Commodities, and REITs, for example, GLI can provide additional diversification to institutional portfolios. With roughly 80 available GLI products in the universe, investors can select from a variety of approaches. The first GLI strategies were incepted in the mid-to-late 2000s and are pre-dated by unlisted infrastructure investment strategies that invested in privately-held companies and assets. Today, investors who seek the benefits of the infrastructure asset class without the liquidity constraints of the unlisted space may find an appropriate solution in GLI.

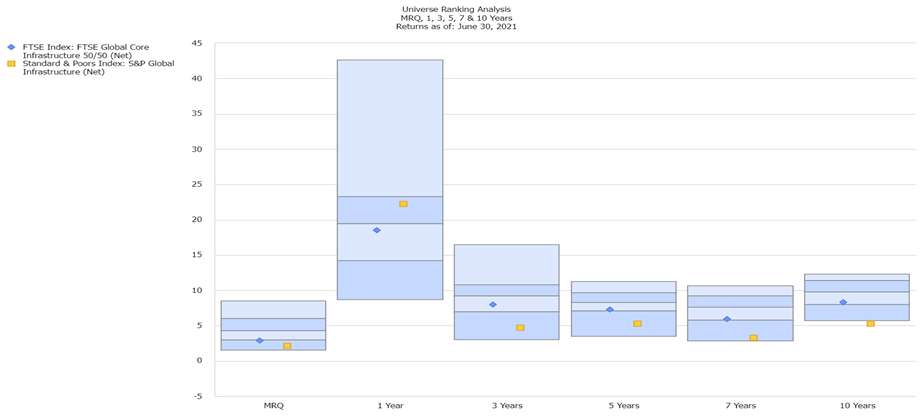

Within the infrastructure universe, performance can vary depending on the investment strategy. The median infrastructure manager has delivered an approximately 8% annualized return over the trailing ten-year period.

In mapping out the GLI universe of securities, asset managers have a degree of overlap in their respective definitions of the asset class. These investment similarities reflect the general agreement around some of the key characteristics that define an infrastructure company, such as high barriers to entry and regulated cash flows. There are certain industries where asset managers may differ in coverage, such as the inclusion of social infrastructure (e.g. schools, hospitals), construction companies, or emerging markets. One of the most important areas of differentiation is the selected benchmark.

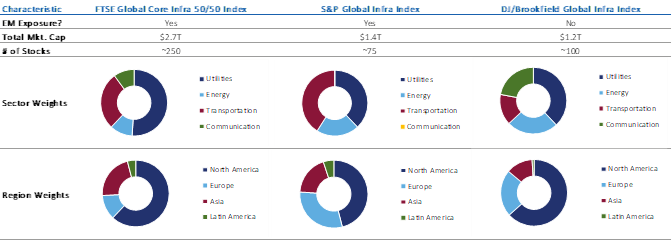

The most commonly used GLI indices include the FTSE Global Core Infrastructure Index, the S&P Global Infrastructure Index, and the Dow Jones Brookfield Global Infrastructure Index. The differences in their characteristics are summarized below (Source: Wilshire, First Sentier), but companies included in these indices are generally involved in the development, ownership, operation, management, and/or maintenance of structures or networks used for the processing or moving of goods, services, information/data, people, energy, or necessities from one location to another (Source: FTSE).

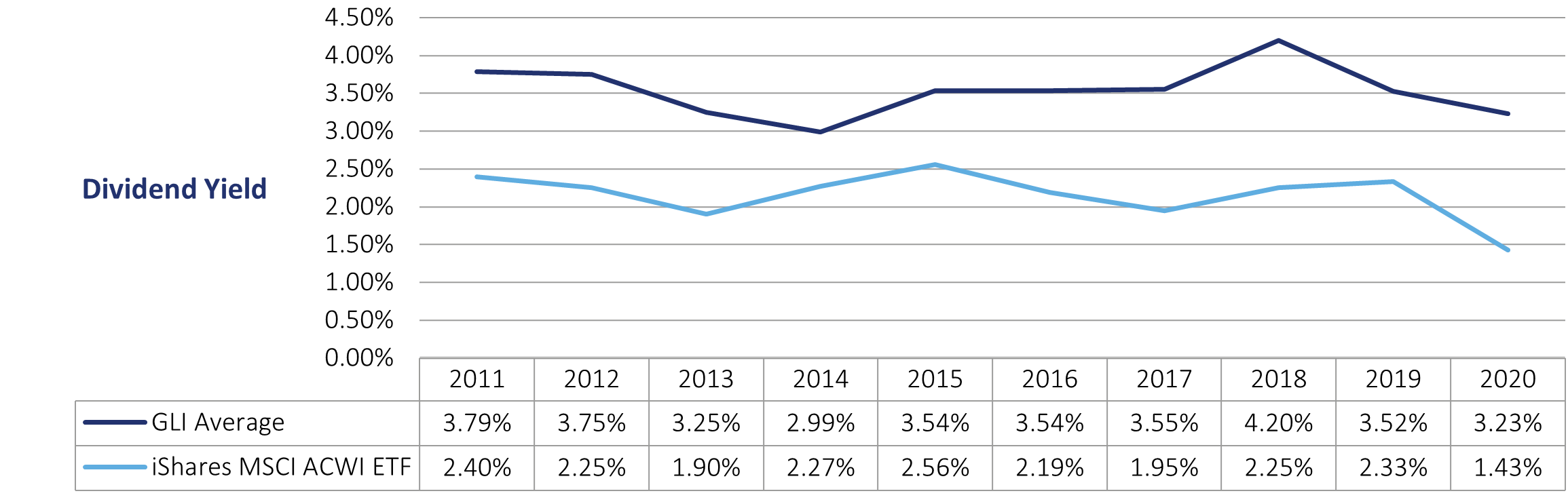

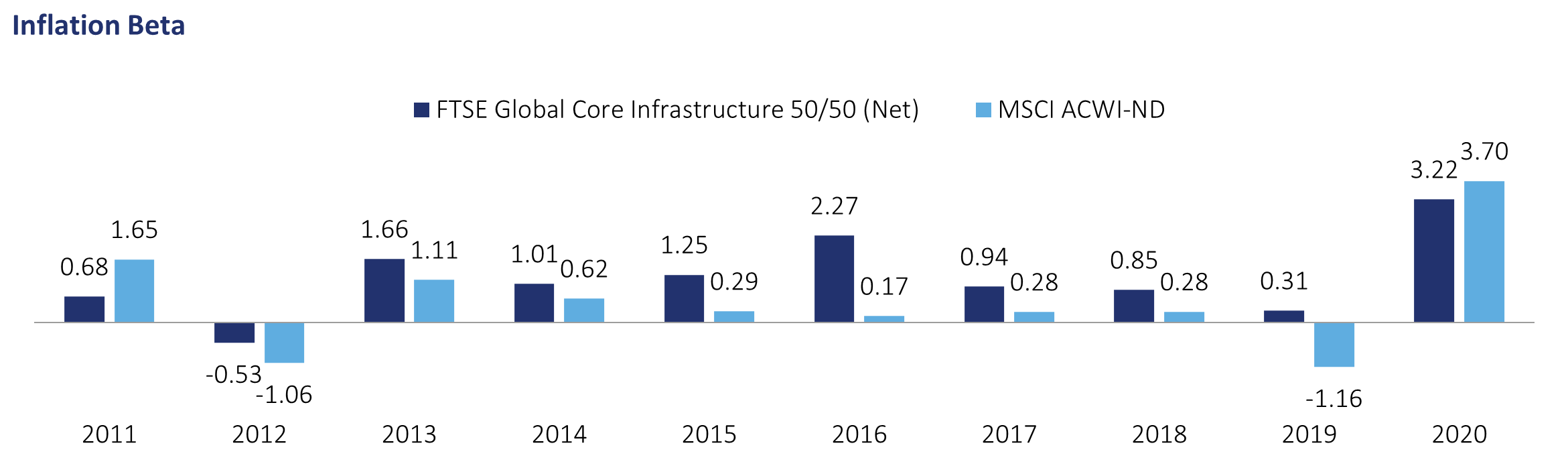

Relative to the broad global equity market, GLI may provide several benefits including an attractive dividend yield, greater inflation sensitivity, and incremental diversification. Since 2011, the FTSE Global Core Infrastructure Index (the GLI Index) has averaged a dividend yield of more than 3% and routinely exceeds that of global equities (iShares MSCI ACWI ETF). Over the same time period, the GLI Index produced a standard deviation of roughly 11.7%, compared with 14% for global equities (Source: Wilshire, eVestment). Many GLI industries generate revenues that are closely tied to inflation such as airports, toll roads, or electric utilities. As a result, GLI has historically exhibited a higher beta to inflation relative to global equities (Source: Wilshire, eVestment).

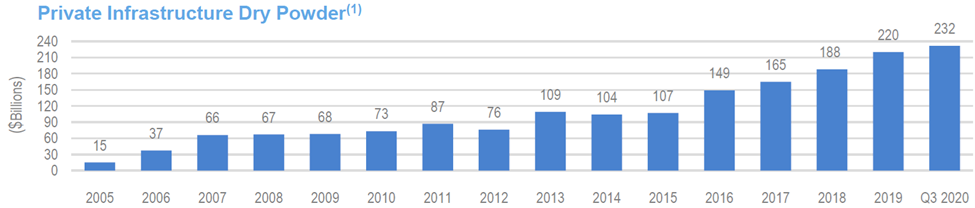

In addition to the improvements that a GLI allocation can bring to a portfolio, the case for GLI is also supported by economic trends such as the shift to renewable energy, the expansion of electric vehicles, the build out of 5G infrastructure, and the global need for infrastructure investment. These are enduring trends that will require a high level of investment over at least the next decade. With an increasing amount of private capital continuing to chase a limited number of investment opportunities (Source: C&S, Preqin), GLI offers exposure to these trends with better liquidity.

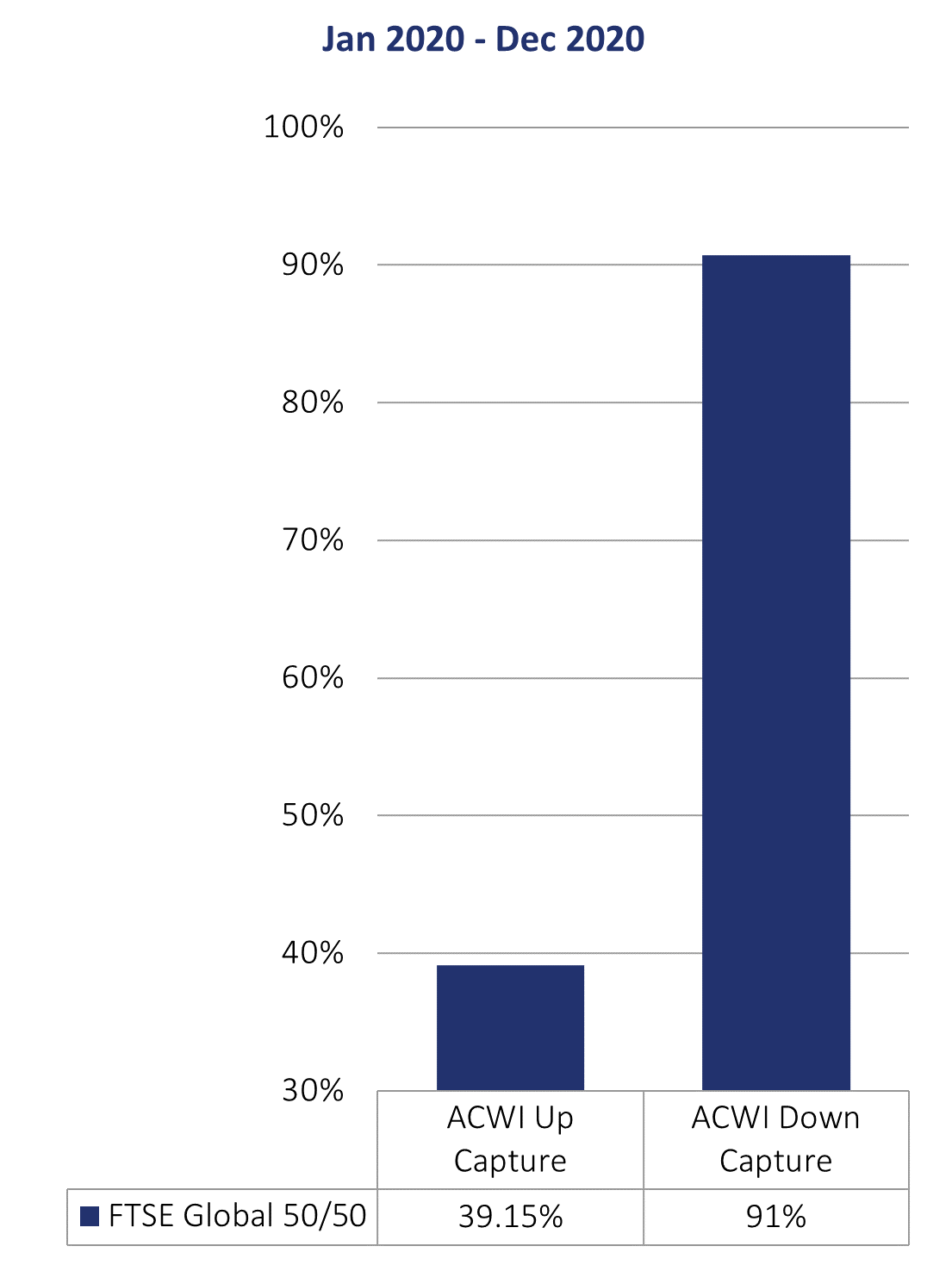

While GLI has historically provided strong downside protection versus the broader equity market, 2020 stands out as a year that had a particularly negative impact on certain infrastructure sectors. While telecommunication industries like cell towers were among the beneficiaries of the shutdown, transportation industries like airports and toll roads experienced some of the worst stock price declines across global equities and heavily weighed on performance of GLI overall. The charts below show the impact that the COVID-19 pandemic had on the upside/downside capture profile of GLI (Source: Wilshire, eVestment).

Despite the 2020 headwinds, the listed infrastructure universe is poised to benefit from enduring economic trends and can enhance the risk/return profile of a diversified portfolio. Additionally, while GLI securities trade as a subset of global equities, investors have an array of options for investment strategies within the GLI universe. Whether the investment strategy seeks inflation sensitivity, targets a dividend yield, incorporates sustainability goals, or growth capture, a GLI allocation can help investors reach their portfolio goals.

About the Author:Cornell McCullom is an Associate with Wilshire and a member of the Traditional Manager Research Group where he focuses on equity and Real Asset strategies. Disclaimers:Wilshire is a global financial services firm providing diverse services to various types of investors and intermediaries. Wilshire’s products, services, investment approach, and advice may differ between clients and all of Wilshire’s products and services may not be available to all clients. For more information regarding Wilshire’s services, please see Wilshire’s ADV Part 2 available at www.wilshire.com/ADV. Wilshire believes that the information obtained from third-party sources contained herein is reliable, but has not undertaken to verify such information. Wilshire gives no representations or warranties as to the accuracy of such information and accepts no responsibility or liability (including for indirect, consequential or incidental damages) for any error, omission, or inaccuracy in such information and for results obtained from its use. This material may include estimates, projections, assumptions, and other "forward-looking statements." Forward-looking statements represent Wilshire's current beliefs and opinions in respect of potential future events. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual events, performance, and financial results to differ materially from any projections. Forward-looking statements speak only as of the date on which they are made and are subject to change without notice. Wilshire undertakes no obligation to update or revise any forward-looking statements. Wilshire Advisors, LLC (Wilshire) is an investment advisor registered with the SEC. Wilshire® is a registered service mark. Copyright © 2021 Wilshire. All rights reserved. Wilshire is a Consultant member of TEXPERS. The views and opinions contained herein are those of the author and do not necessarily represent the views of Wilshire nor TEXPERS. These views are subject to change.Follow TEXPERS on Facebook, Twitter and LinkedIn for the latest news about Texas' public pension industry.