Reading Fed Tea Leaves? Watch Market Prices Instead

|

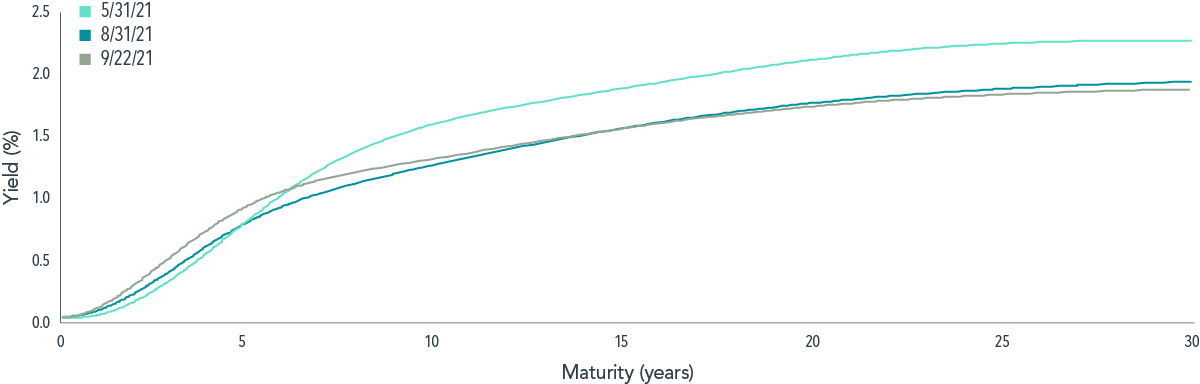

Fed watching is once again one of the markets’ favorite pastimes. Federal Reserve officials continue to signal that they would favor tapering of bond purchases in 2021, in line with recent announcements from the European Central Bank. When and how remain to be seen. With ample speculation about the Fed, unemployment, and inflation, it might be a good time for a reminder about what Fed announcements can, and cannot, tell us about the future of fixed income markets. Yields reflect the aggregate expectations of all market participants, including opinions on how and when the Fed will act. And even if a crystal ball could reveal the timing and direction of the Fed’s actions, we would not know how broader interest rates would react. The Fed is one of many market participants in a larger ecosystem that impacts yield curves at large. Fed Says ‘Jump,’ Market Says ‘Not So Fast’ At the Federal Open Market Committee meeting in July, Fed officials strongly suggested they would soon slow bond purchases, and they confirmed their intentions at the Jackson Hole Symposium last month. This week, Fed Chair Jerome Powell announced that “a moderation in the pace of asset purchases may soon be warranted.”[1] But fixed income markets have responded tepidly, perhaps because market participants already priced in a potential tapering. Exhibit 1 shows that interest rates generally decreased during the last three months, as opposed to increasing like they did when the Fed announced tapering in the wake of the Global Financial Crisis (“GFC”). This movement may suggest that market dynamics and participants in aggregate, not the Fed alone, determine the level and shape of the yield curve. |

EXHIBIT 1Hop, Skip, or Jump: Always Aggregating InformationTreasury yield curve, May 31, August 31, and September 22, 2021 [1] “Federal Reserve Issues FOMC Statement,” Federal Reserve, September 22, 2021. [1] “Federal Reserve Issues FOMC Statement,” Federal Reserve, September 22, 2021.

Source: Barclays |

|

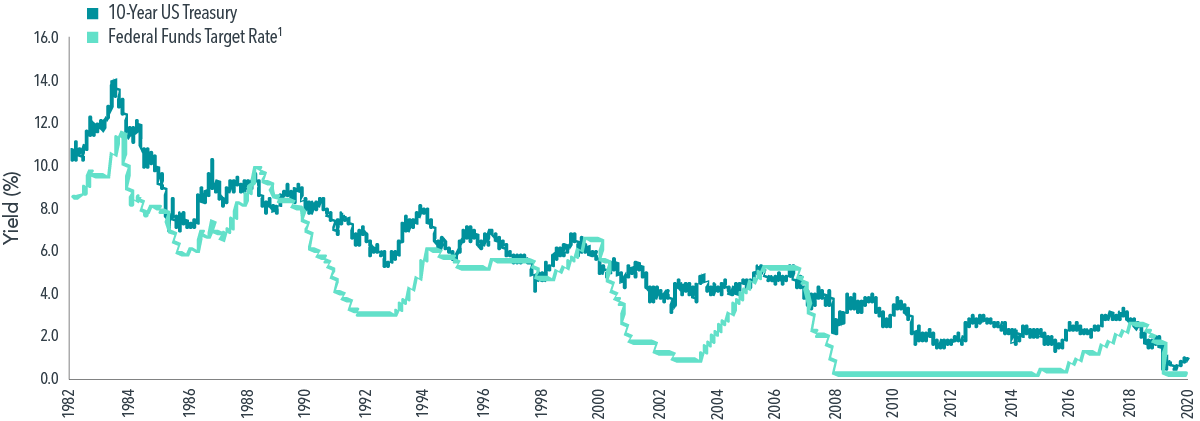

While shorter-term yields rose, longer-term yields fell, a reminder that longer-term yields do not always move in lockstep with changes in the federal funds target rate. Exhibit 2 shows there have been instances when the Fed increased the federal funds target rate, yet longer-term interest rates decreased. From January 1983 to December 2020, there were 70 months in which the federal funds rate increased. About a third of the time, the increase coincided with a decrease in the 10-year US Treasury yield. The lack of a consistent relation between movements in long-term yields and the federal funds rate reinforces the notion that yield curves reflect all available market information, including any Fed action. |

EXHIBIT 2A Tenuous Relation10-year US Treasury yield vs. federal funds target rate, January 1983-December 2020 1. The federal funds rate refers to the rate that depository institutions charge each other for an uncollateralized overnight loan of funds. The Federal Reserve sets the target for this interest rate, though market forces can cause variation from the target rate at times.Source: US Treasury data provided by FRED, Federal Reserve Bank of St. Louis.Data is subject to change. 1. The federal funds rate refers to the rate that depository institutions charge each other for an uncollateralized overnight loan of funds. The Federal Reserve sets the target for this interest rate, though market forces can cause variation from the target rate at times.Source: US Treasury data provided by FRED, Federal Reserve Bank of St. Louis.Data is subject to change. |

|

Investors should not discount the importance of the Fed and its role in the global financial markets, however. The Fed has many powerful tools to simulate the economy during times of economic distress, as evidenced by its response to the GFC and the COVID-19 pandemic. Still, the Fed does not act in a vacuum. Prices across the broader yield curve are set in conjunction with the aggregate expectations of numerous other market participants. No Reliable Way to Predict Future Interest Rates Investors don’t need to dedicate time or resources to predicting the Fed’s next move. Rather, decades of empirical research provide a framework for understanding how to use information in market prices and diversification to pursue higher expected returns and improve the reliability of outcomes. Larger differences in forward rates among bonds of different durations, credit qualities, or currencies of issuance can indicate larger differences in expected returns. Using market information available in global yield curves is a more reliable way to improve expected returns than trying to read the Fed’s tea leaves. |

| Sources:[1] “Federal Reserve Issues FOMC Statement,” Federal Reserve, September 22, 2021. |

About the Authors: Sooyeon Mirda, CFA, is an Investment Strategist in Dimensional’s Investment Solutions Group. Based in the Austin office, Mirda is a member of the Product Specialists team and serves as a subject matter expert on the firm’s fixed income investment philosophy and strategies. She supports the firm’s fixed income efforts by communicating with clients, prospects, and various intermediaries about their portfolios. In addition, she writes commentary, develops internal and external content on portfolio management and strategies, and is involved with internal training for various distribution channels. Before returning to Dimensional, Mirda worked for Goldman Sachs in San Francisco, where she managed portfolios and developed creative investment solutions for ultra-high-net-worth clients, foundations, and endowments. Before this, she worked for Dimensional as an Associate Investment Strategist in fixed income. Prior to originally joining Dimensional, Mirda was part of a fixed income rotational program at AllianceBernstein in New York City, where she focused on credit research and bond portfolio management. A CFA® charterholder, Mirda graduated with honors from Princeton University with a bachelor’s degree in economics and minor in finance. Sooyeon Mirda, CFA, is an Investment Strategist in Dimensional’s Investment Solutions Group. Based in the Austin office, Mirda is a member of the Product Specialists team and serves as a subject matter expert on the firm’s fixed income investment philosophy and strategies. She supports the firm’s fixed income efforts by communicating with clients, prospects, and various intermediaries about their portfolios. In addition, she writes commentary, develops internal and external content on portfolio management and strategies, and is involved with internal training for various distribution channels. Before returning to Dimensional, Mirda worked for Goldman Sachs in San Francisco, where she managed portfolios and developed creative investment solutions for ultra-high-net-worth clients, foundations, and endowments. Before this, she worked for Dimensional as an Associate Investment Strategist in fixed income. Prior to originally joining Dimensional, Mirda was part of a fixed income rotational program at AllianceBernstein in New York City, where she focused on credit research and bond portfolio management. A CFA® charterholder, Mirda graduated with honors from Princeton University with a bachelor’s degree in economics and minor in finance.  Marilyn Giselle Hazlett is an Analyst in Dimensional’s Austin office. She is a part of the product management team within the firm’s Investment Solutions Group, which is responsible for supporting the effective communication of Dimensional’s investment approach and its strategies to clients and prospective clients. Hazlett works across a range of Dimensional’s product initiatives and strategies with a focus on written materials. She holds a bachelor’s degree in economics from Clemson University. Marilyn Giselle Hazlett is an Analyst in Dimensional’s Austin office. She is a part of the product management team within the firm’s Investment Solutions Group, which is responsible for supporting the effective communication of Dimensional’s investment approach and its strategies to clients and prospective clients. Hazlett works across a range of Dimensional’s product initiatives and strategies with a focus on written materials. She holds a bachelor’s degree in economics from Clemson University. |

| Disclosures:Dimensional Fund Advisors is an Associate member of Texas Association of Public Employee Retirement Systems (TEXPERS). Dimensional and TEXPERS are separate, unaffiliated entities. The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized copying, reproducing, duplicating, or transmitting of this document are strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein. RISKSInvestments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful. Diversification neither assures a profit nor guarantees against loss in a declining market. UNITED STATES: Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission. Follow TEXPERS on Facebook, Twitter and LinkedIn as well as visit our website for the latest news about Texas' public pension industry. |