|

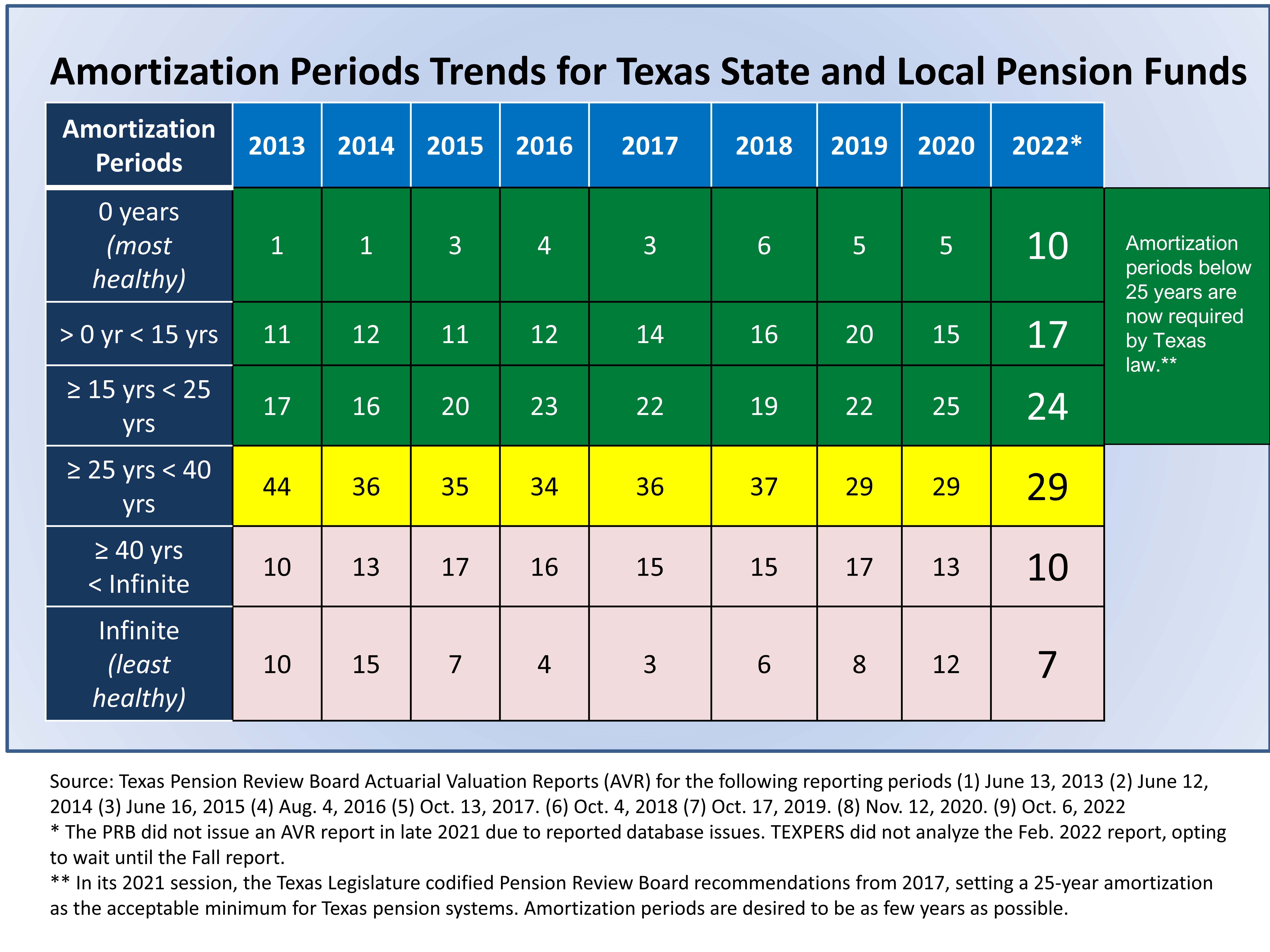

2022 SPECIAL REPORT Texas Public Employee Pension Funds Set Record in Achieving Legislature’s More Stringent RequirementsPension Funds Continued Positive Trend of Lowering Amortization Period The 100 state and local pension funds that report financial statistics to the Texas Pension Review Board combined in 2021-22 to improve their aggregate amortization periods in record-breaking fashion, according to a TEXPERS study of PRB data. Fifty-one (51) pension funds achieved the Pension Review Board’s recommended amortization period of 0-25 years, the highest most attaining this recommended level in at least the last 10-years for which TEXPERS has consistent records from the PRB.*

The amortization period, which can be compared for illustration to the years left to pay on a home mortgage, is the PRB’s single “most appropriate” measure of public retirement systems’ health.** However, this report seeks to advise that amortization periods are certainly not the only measure of pension fund health, and the Pension Review Board in recent years has developed other tests to trigger “Intensive Reviews.” These PRB evaluations help detect whether certain signs might be giving warning signs before worrisome amortization period changes occur. TEXPERS Summaries on the Amortization periods:

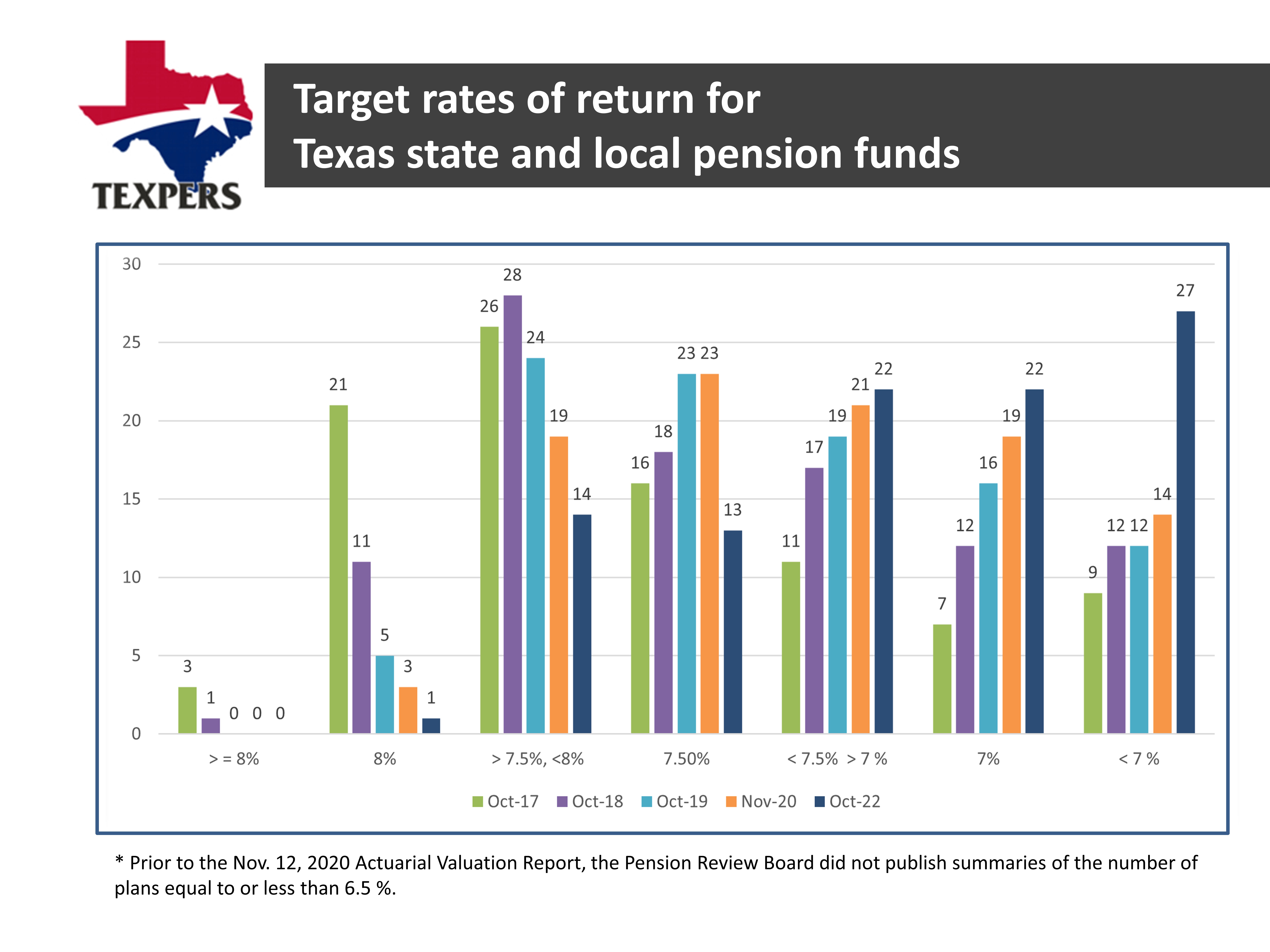

Target Rates Continue Trending Lower The Pension Review Board’s October 6, 2022, Actuarial Valuation Report continued to demonstrate pension funds’ conscious effort to reduce target/discount rates. These are the return targets they set for investment portfolio performance. Lowering system target rates helps pension systems manage their investments in more conservative ways, but sometimes require additional contributions from public employees and/or their governmental-employer sponsor. Key observations for the last year are:

The Pension Review Board has informally advised systems that lowering target rates will help them align their forecasts to guidance from industry experts, that domestic and global capital markets will have generally lower returns for the foreseeable future.

TEXPERS Executive Director Art Alfaro offered the following comments: “This is indisputably the best overall set of data we’ve seen regarding the aggregate health of Texas’ state and local pension funds. Clearly, the public policies that have been put in place over the long-term by the Texas Legislature are working to achieve intended results. “Like the last report in 2020, the most promising testament to pension fund management is that amortization periods continued to improve despite while there were serious continuing efforts to lower target rates for investment returns. With the market declines of 2022, this conservative effort will keep pension funds healthy. “The data confirms that Texas pension funds worked hard in the last year to follow the direction set by the state Legislature in 2021, to improve the various metrics of pension fund health. These significant upgrades are not easily achieved – they require careful coordination by the funds’ Boards, their city sponsors and their members. In the last year, we’ve seen exemplary progress from systems in Amarillo, Conroe, Denton, Irving, Longview, San Angelo and Texarkana. These improvements should not go unnoticed by lawmakers and the public alike.” The Legislature passed House Bill 3898 in 2021 adopting Pension Review Board recommendations to reset the amortization period trigger for Funding Soundness Restoration Plans. The bill moved the target period to 30 years, from 40 years, which the PRB contends is more appropriate to current actuarial standard practices. Art Alfaro may be reached for comment by emailing Joe Gimenez at [email protected] or calling 713.478.8034. More graphics are available at 2022 Amortization Trend Charts. _______________________________________________________________________________________ * This report shows data from 2013, but our analysis for this headline and report includes data from 2011-2022. ** The PRB defines amortization period as “the length in time, in years, needed to pay for the unfunded actuarial accrued liability (UAAL) and reflects a system’s ability to pay its normal cost plus UAAL.” UAAL is the present value of benefits earned to date that are not covered by plan assets and normal cost is the portion of cost of projected benefits to the current year. |